Transferring a family farm business to the next generation can be a complex and often emotionally charged endeavour. The introduction of Bill C-208 brought significant changes to the rules governing intergenerational farm transfers, impacting how farm families plan for the future. These changes, set to take effect on January 1, 2024, have sparked discussions around the challenges and opportunities they present for farm families navigating the intricacies of succession planning.

What were the previous rules?

Farm businesses that are transferring the shares of their family farm intergenerationally can treat the gain on the sale as taxable gains (which are 50% taxable) rather than fully taxable dividends (as was the case before Bill C-208 was introduced).

According to Miller Thomson’s article New Taxation rules impacting transfers of family businesses to the next generation:

- Prior to the changes to Section 84.1 of the Income Tax Act (ITA) it was more tax-efficient for parents to sell the business to a third party rather than to their children.

- Specifically, where a parent sold the shares of a family business corporation to her child’s corporation, what would have been the parent’s capital gain on the sale was converted to a dividend and taxed at the higher dividend tax rates.

- Further, where a parent sold the shares directly to her child and utilized her lifetime capital gains deduction to shelter the gain from tax, and the child later sold the shares to a related corporation, the child would face the same dividend tax treatment, to the extent of the parent’s sheltered gain.

- Thus, the rule effectively penalized families where a child used a corporation to finance the transaction in an effective manner. And this was so even when the child was paying full market value for the shares.

- This contrasts with the tax treatment that the parent would have received if she sold those same shares to an arm’s length third party.

At the heart of the matter, section 84.1 worked to stop corporations from stripping corporate surplus by selling shares to another corporation related to the individual:

“Section 84.1 of the Act is an anti-avoidance rule. It is designed to prevent corporate surplus that would be taxed at dividend tax rates, if that surplus were distributed to a taxpayer as a dividend, from being converted into a capital gain taxed at (lower) capital gains tax rates. Section 84.1 applies where an individual sells shares of a Canadian corporation to another corporation related to the individual.”

Source: Miller Thomson, New taxation rules impacting transfers of family businesses to the next generation Everything you thought you knew about intergenerational transfers is now wrong, June 2021

What are the rules today?

Businesses can be transferred to corporations related to the individual at a preferential tax rate.

- The changes made to section 84.1 were designed to overcome the perceived inequity whereby a seller of the shares of such businesses to arm’s-length third parties receives more favourable tax treatment than she would if she sold those same shares to the next generation of the family

- In adjusting the rules to allow for corporations to sell to another corporation related to the seller, there was an unintended consequence of allowing corporate surpluses to be stripped at the preferential capital gains tax rate (as compared to dividends). This was true for all transfers even if not to a child.

- To address this unintended consequence, amendments to Bill C-208 have been proposed to be effecting on or after January 1, 2024.

Case Study

The van Persies, owners of a South Western Ontario farm, have a strategic plan in motion. They are set to sell this farm to two of their adult children in June 2024, leveraging the changes to section 84.1 of the Income Tax Act to their advantage.

Currently, the van Persies personally own shares of their family farm corporation. In their planned transfer, they will sell these shares to a corporation owned by their two children. Assuming they have not previously used it, selling shares of their corporation allows both parties to take advantage of the Lifetime Capital Gains Exemption (LCGE). This exemption allows them to shield the first $2 million in gains on the farm from taxation. Furthermore, any remaining gains beyond the $2 million threshold will be treated as a capital gain and not taxed at the higher dividend rate as they would have been prior to Bill C-208.

| Prior to Bill C-208 | With Bill C-208 | |

| Fair Market Value of Farm | $22,000,000 | $22,000,000 |

| Adjusted Cost Base of Farm | $2,000,000 | $2,000,000 |

| Gain on Sale | $20,000,000 | $20,000,000 |

| Lifetime Capital Gains used | $0 | $2,000,000 |

| Net Gain on Sale | $20,000,000 | $18,000,000 |

| Tax Treatment of Sale Proceeds | Dividend | Capital Gains (50% inclusion rate) |

| Tax rate (Ontario) | 48% | 27% |

| Taxable Proceeds | $20,000,000 | $9,000,000 |

| Tax Payable | $9,600,000 | $4,860,000 |

| Net after-tax proceeds to selling parents | $12,400,000 | $17,140,000 |

| Net advantage | $4,740,000 |

What’s changing?

According to Grant Thorton’s article Intergenerational business transfers: Proposed changes you should know from April 2023:

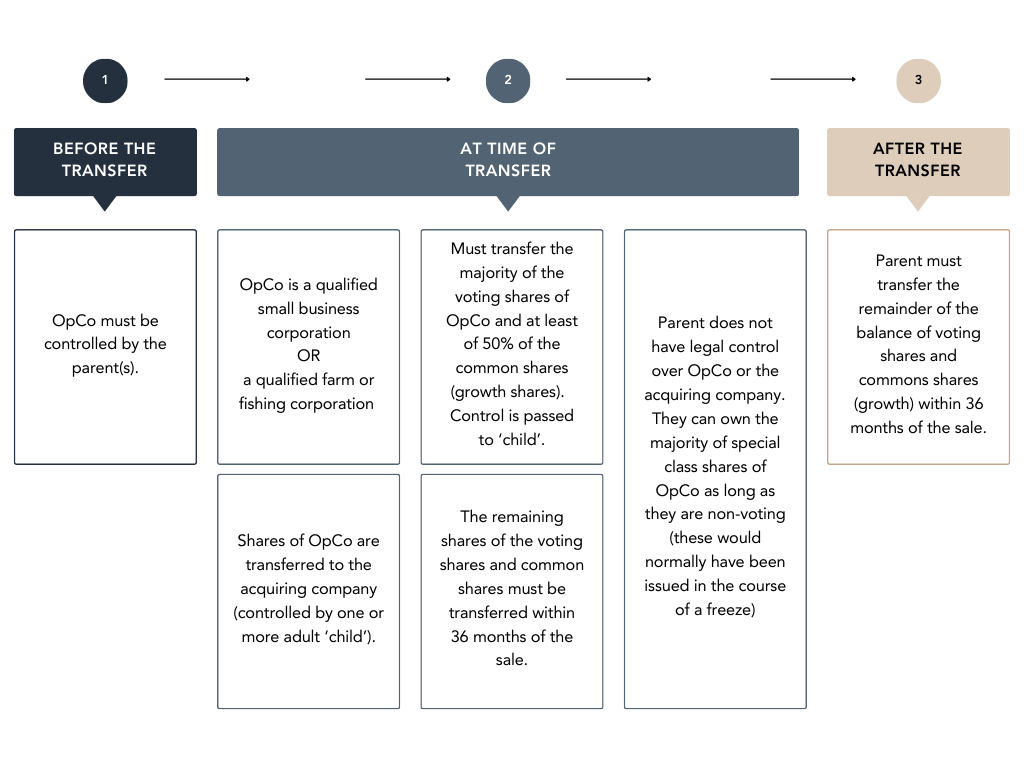

- The proposed changes to the Intergenerational Business Transfers (IBT) rules include new timing requirements to specify when the parent must give up control of the transferred business and when the adult child or grandchild (or a niece/nephew or grandniece/grandnephew for transactions on or after January 1, 2024) whose corporation acquires the shares of the business must have active involvement in the business.

- These changes, introduced in Budget 2023, are intended to ensure that the rules only apply to genuine IBTs and prevent “surplus stripping”.

Furthermore , the new measures include two options for IBTs:

- an immediate IBT (three-year test)

- a gradual IBT (five-to-ten-year test)

The IBT must also meet the following conditions:

| Proposed condition | Immediate IBT (Three-year test) | Gradual IBT (Five to ten-year test) |

| Transfer of control and economic interest | Parent can’t have legal or factual control (e.g., economic or other influence) after the share transfer | Parent can still have economic influence, but not legal control after the share transfer. However, Parent must reduce their debt and equity interests in OpCo and AcquireCo within 10 years of the share transfer to: 30% of their value for QSBCs 50% of their value for QFFCs |

| Transfer of Management (Management test) | Within 36 months of the share transfer, or longer if reasonable | Within 60 months of the share transfer, or longer if reasonable |

| Child retains control of business | Child(ren) retains legal control for at least 36 months after the share transfer | Child(ren) retains legal control for the greater of: 60 months, or until the business transfer is completed |

| Child works in the business (Engagement test) | At least one child remains actively involved for the 36 month period | At least one child remains actively involved for the greater of: 60 months, or until the business transfer is completed |

| Active business | Each relevant business of OpCo must be carried on an active business for the 36 month period | Each relevant business of OpCo must be carried on an active business for the greater of: 60 months, or until the business transfer is completed |

The changes to section 55 expand the scope of related-party reorganization transactions to facilitate such reorganizations on a tax-effective basis within an expanded family unit.

Case Study Continued

Let’s return to the van Persies and examine how these changes impact their situation. While these changes won’t alter their bottom-line proceeds leading up to their planned sale in June 2024, the van Persies must now navigate the intricacies of the updated criteria for both immediate and gradual business transfers. In particular, they need to carefully consider how these changes will affect the timing of relinquishing control to their children.

As you navigate the evolving landscape of intergenerational business transfers, remember that there are steps you can take before determining which transfer option best fits your unique circumstances. If you find yourself in need of guidance or assistance, don’t hesitate to reach out. We can connect you with the right experts and resources to help you make informed decisions.

As you embark on this journey, keep in mind that the key lies in strategic planning, compliance with the new criteria, and a deep understanding of how these tax changes will affect the timing of relinquishing control to the next generation. Getting started is the first step towards securing the future of your family business for generations to come.

Sources

The views expressed in this commentary are those of Tall Oak Capital Advisors as at the date of publication and are subject to change without notice. This commentary is presented only as a general source of information and is not intended as a solicitation to buy or sell specific investments, nor is it intended to provide tax or legal advice. Statistics, factual data and other information are from sources Tall Oak believes to be reliable but their accuracy cannot be guaranteed. This commentary is intended for distribution only in those jurisdictions where Tall Oak Capital Advisors are registered. Securities-related products and services are offered through Raymond James Correspondent Services Ltd., member Canadian Investor Protection Fund. Insurance products and services are offered through Gryphin Advantage Inc., which is not a member-Canadian Investor Protection Fund. This commentary may provide links to other Internet sites for the convenience of users. Tall Oak Capital Advisors is not responsible for the availability or content of these external sites, nor does Tall Oak Capital Advisors endorse, warrant or guarantee the products, services or information described or offered at these other Internet sites. Users cannot assume that the external sites will abide by the same Privacy Policy which Tall Oak Capital Advisors adheres to.